Life Insurance for Marijuana Users: The 2026 Ultimate Guide to Non-Smoker Rates

Key Takeaways

Yes, many marijuana users can qualify for Standard or even Preferred non-smoker life insurance rates in 2026. Pricing depends primarily on frequency of use, consumption method, and overall health.

- 1–2 times per month: Often competitive for Preferred or Preferred Plus at marijuana-friendly carriers.

- 2–3 times per week: Commonly eligible for Standard Non-Smoker, depending on the carrier.

- Daily use: Frequently results in Smoker rates or Table ratings, though coverage is still available.

- Edibles are generally viewed more favorably than smoking or vaping.

- For medical marijuana, the underlying health condition usually drives the rate class more than cannabis itself.

- Full disclosure on your life insurance application is critical to avoid claim issues during the contestability period.

The final rate class is determined by a full underwriting review and varies by carrier, health profile, and state.

Introduction

Disclaimer: This guide is for educational purposes only. Underwriting outcomes vary by carrier, individual health profile, and state of residency. Nothing here constitutes a guarantee of a specific rate class. All rates are subject to full medical review by the issuing life insurance company.

If you’ve been holding off on getting life insurance because you use marijuana, you might be following old rules. It used to be true that using cannabis meant you were automatically charged “smoker rates,” which could double or even triple your monthly bill. In 2026, that has changed.

Over the last ten years, the insurance industry has shifted. Because marijuana is now legal in most states, insurance companies have better data and have updated their rules.

Today, many life insurance companies treat marijuana users the same as people who don’t use it. Depending on how often you use it, how you consume it (like edibles versus smoking), and your general health, you can now qualify for the best, most affordable “non-smoker” rates.

For example, Lincoln Financial explicitly classifies marijuana as a non-tobacco product in its underwriting guidelines. This means you can get the lower non-tobacco prices right away, rather than needing a special exception.

This isn’t just another overview. We’re pulling back the curtain on how underwriters actually grade cannabis use in 2026, which carriers are currently the most aggressive on rates, and the exact steps you need to take to secure a non-smoker policy.”

How Life Insurance Underwriting Actually Works for Marijuana Users

The Underwriting “Golden Rules”

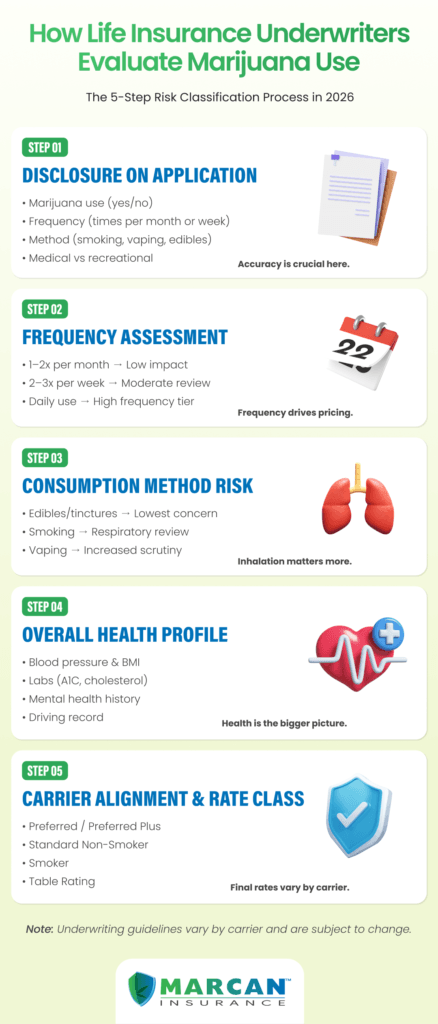

Before diving into frequency tables and carrier comparisons, it’s important to understand the framework underwriters apply. Life insurance underwriting is fundamentally a risk classification exercise. Every applicant is sorted into a rate class – from Preferred Plus (lowest risk, lowest premium) down through Standard, Substandard (Table Ratings), and Declined.

For marijuana users, underwriters are asking four core questions:

- How often do you use? (Frequency drives the rate class more than almost any other factor)

- How do you consume? (Smoking, vaping, edibles, and tinctures are treated differently)

- Why do you use? (Recreational vs. medical marijuana, both carry distinct underwriting implications)

- What does the rest of your health profile look like? (A healthy, occasional user is a very different risk than a daily user with comorbidities)

The THC factor: What happens if THC is found in the insurance medical exam?

Some term life insurance policies above $100,000 will require an insurance medical exam. This exam consists of a brief nurse-administered visit that includes a blood draw, urinalysis, blood pressure measurements, height/weight measurements, and a health questionnaire.

THC is detectable in urine for a wide window depending on the frequency of use:

| Usage Pattern | Approximate Detection Window |

| Single use (1 time) | 3-4 days |

| Occasional (a few times/month) | 5-10 days |

| Moderate (several times/week) | 10-21 days |

| Daily/heavy use | 30-60+ days |

Detection windows sourced from peer-reviewed urinary cannabinoid excretion research (Huestis et al., PubMed; PMC3461262; PMC2763020). Actual results vary based on individual metabolism, body fat percentage, and test cutoff thresholds.

Here is the critical point most guides miss: a positive THC result on your exam does not automatically mean smoker rates. What it means is that your disclosed usage, or lack of disclosure, will be scrutinized against what the lab shows.

If you disclosed marijuana use on your application and THC appears in your urinalysis, underwriters treat this as expected and evaluate you accordingly. If you didn’t disclose and THC appears, that is a material misrepresentation — a serious problem discussed in detail below.

Some carriers additionally test for cotinine (the metabolite of nicotine). A positive cotinine result combined with THC, indicating both tobacco and marijuana use, will commonly result in tobacco/smoker rate classification regardless of your cannabis frequency.

Consumption Methods: Why How You Use Matters as Much as How Often

The life insurance industry doesn’t just care that you use cannabis. It cares how you use it, because the delivery method correlates to different health risks.

Smoking Marijuana

Smoking marijuana is the most scrutinized consumption method. Inhaled combustion, whether tobacco or cannabis, introduces the same irritants, carcinogens, and pulmonary stress.

Many underwriters apply a respiratory risk lens to cannabis smokers similar to cigarette smokers, particularly if use is frequent. Some carriers classify daily cannabis smokers in a smoker rate class purely based on inhalation method, independent of nicotine use.

Vaping Cannabis

Counterintuitively, vaping cannabis is often treated more harshly than smoking by some underwriters in 2026. The lung injury outbreak (EVALI) associated with vaping in recent years, particularly with THC vape cartridges containing vitamin E acetate, has made underwriters cautious.

Several carriers that offer Standard Non-Smoker rates to occasional cannabis smokers will decline or table-rate applicants who vape cannabis concentrates. This is an area where carrier selection is especially important.

Edibles and Tinctures

Edibles, capsules, tinctures, and other non-inhaled methods are generally viewed most favorably by life insurance underwriters.

Because these methods carry no pulmonary risk, an applicant who uses cannabis edibles occasionally and is otherwise healthy has a strong argument for Preferred or Standard Non-Smoker classification at marijuana-friendly carriers. This is an underwriting nuance that most applicants and even many agents are unaware of.

The simplest upgrade a marijuana user can make before applying for life insurance is switching from smoking or vaping to edibles. Same frequency, meaningfully better underwriting outcome at most carriers.

Medical Marijuana vs. Recreational Use: The Underlying Condition Is What Drives the Premium

This is arguably the most misunderstood aspect of life insurance for marijuana users. Many applicants with a medical marijuana card assume the prescription itself is the primary underwriting concern. In reality, the underlying health condition being treated is what underwriters focus on.

A medical marijuana cardholder using cannabis to manage mild chronic pain or insomnia may face little additional underwriting scrutiny beyond the cannabis use itself. A cardholder using it to manage severe Crohn’s disease, multiple sclerosis, or cancer-related symptoms will face underwriting for those conditions, and the marijuana is almost incidental.

Practical implication: If you have a medical marijuana card, be prepared to fully disclose and document the condition for which it was prescribed. An experienced independent agent can help you identify carriers whose underwriting is most favorable for your specific combination of health condition and marijuana use.

The Frequency Table: The Heart of Marijuana Underwriting in 2026

This is the section that competitors consistently get wrong by using vague terms. Here is how weekly and monthly usage typically map to rate classes at marijuana-friendly carriers. Note that these are commonly observed outcomes (not guarantees), and they assume an otherwise clean health profile.

| Frequency | Rate Class (Commonly Seen) | Carrier Examples |

|---|---|---|

| 1–2x per month | Preferred Plus / Preferred Best | Lincoln Financial, Prudential |

| 3–4x per month | Preferred to Standard Non-Smoker | Corebridge, Prudential, Lincoln |

| 2–3x per week | Standard Non-Smoker | Corebridge, select regional carriers |

| 4–6x per week | Standard Smoker / Table Rating | Varies widely by carrier |

| Daily | Smoker Rate or Table | Narrow carrier options |

*These outcomes assume no tobacco use, excellent overall health, a clean driving record, and full underwriting approval. The issuing life insurance company determines the final rate class.

To get an accurate estimate of your life insurance premium, use the INSTANT QUOTES calculator on this page. Share your specific details with our team, and we’ll help identify the life insurance company most likely to offer your strongest possible rating and most competitive pricing.

Occasional Use: 1–2 Times Per Month

Commonly seen rate class: Preferred Best / Preferred Plus

Applicants who use marijuana 1–2 times per month and meet all other Preferred underwriting criteria are often competitive for top non-smoker rate classes at marijuana-friendly carriers. This is a significant shift from industry norms of even five years ago.

At some marijuana-progressive carriers, occasional use may be viewed similarly to moderate alcohol consumption, provided no other risk factors are present. This is a lifestyle factor that is noted but doesn’t materially change the mortality risk assessment.

The key requirements at this frequency will be non-smoker status (no tobacco), no DUI history, no other substance use issues, and otherwise excellent overall health markers on the insurance medical exam.

Social Use: 2–4 Times Per Week

Commonly seen rate class: Standard Non-Smoker to Preferred

If you use marijuana 2–4 times a week, your choice of insurance company matters more than ever. Some ‘progressive’ companies will give healthy users a Standard Non-Smoker rate. However, more conservative companies might charge you expensive ‘Smoker’ rates or even deny your application entirely.

Picking the wrong company can be a costly mistake. For example, a 35-year-old using cannabis three times a week could end up paying 60% to 90% more every year just by choosing a conservative carrier over a marijuana-friendly one.”

Daily Use: 7+ Times Per Week

Commonly seen rate class: Standard Smoker to Table Rating

Daily marijuana usage, regardless of consumption method, will commonly result in a Smoker rate classification or a Table Rating (substandard) at most carriers. Some carriers will not offer coverage at all for daily users, particularly if there are any other adverse health or lifestyle factors.

Daily users are not uninsurable. But the carrier universe narrows considerably, the rate class will be less favorable, and the underwriting process will be more intensive. An independent broker who specializes in high-risk underwriting is essential in this scenario.

As a rule of thumb: Marijuana users who consume four times per month or fewer, use non-inhaled methods, and have no tobacco history are competitive for Standard Non-Smoker rates or better at progressive carriers in 2026.

Carrier Spotlight: Who Is Actually Marijuana-Friendly in 2026?

Not all carriers are created equal when it comes to life insurance for marijuana users. Here are three commonly referenced marijuana-progressive carriers:

Please understand that underwriting guidelines change frequently, and this should be verified with a current carrier filing or an experienced broker.

Lincoln Financial Group

Lincoln has been one of the more consistently cannabis-progressive major carriers. Their underwriting guidelines have historically allowed occasional users (up to 2x/month) to be considered for their top non-smoker rate classes, provided all other health criteria are met. Lincoln is a strong first-look option for applicants with low-frequency use and strong overall health profiles.

Prudential

Prudential is one of the few major carriers with published, frequency-specific marijuana criteria. Use of three or fewer times per week qualifies for Non-Smoker rates; four to six times per week typically results in a Table B rating; seven or more times per week results in a decline.

Prudential only gives “smoker rates” to people who smoke cigarettes. This means if you are honest about using marijuana on your application, you can still get the cheaper “non-smoker” price even if your medical exam shows THC in your system. However, there is one strict rule: if you don’t tell them you use marijuana and it shows up in your medical test, they will automatically reject your application.

Corebridge Financial (Formerly AIG Life & Retirement)

Corebridge (the rebranded life and retirement arm of AIG) offers competitive options for moderate users. Underwriters commonly cite them as a carrier willing to offer Standard Non-Smoker rates to applicants using cannabis up to several times per week, depending on the full health profile. Their medical exam requirements and underwriting depth are standard for the industry.

Important note: Underwriting guidelines are proprietary and subject to change. Always work with a licensed independent broker who is up to date on carrier guidelines, rather than relying solely on public information.

Honesty and the Contestability Period: Why Lying on Your Application Is Never Worth It

This section is not optional reading. If you take one thing from this guide, let it be this.

Every life insurance application includes a contestability period, typically 2 years from the policy’s issue date. During this window, if you die, the life insurance company has the legal right to investigate your application for material misrepresentations before paying a claim. If they find that you lied about marijuana use, tobacco use, health conditions, or any other material fact, they can deny the claim entirely and refund only the premiums paid.

The consequences of non-disclosure are not theoretical. Claims investigations routinely include:

- Review of your MIB (Medical Information Bureau) file

- Pharmacy records

- Attending physician statements

- Social media (yes, this is used)

- Toxicology reports in the event of accidental death

If you use marijuana and you are afraid to disclose it, the right answer is not to lie; it is to find the right carrier. As this guide has outlined, there are legitimate pathways to affordable life insurance at Standard Non-Smoker rates or better for many cannabis users. An experienced independent broker can navigate that landscape for you. A claim denial cannot be undone.

Affordable Life Insurance Options: A Comparison Overview

Here is a framework for comparing your options as a marijuana user:

| Policy Type | Exam Required? | Marijuana Notes | Best For |

|---|---|---|---|

| Fully Underwritten Term | Yes | Best rate classes available; full carrier flexibility | Occasional to moderate users in good health |

| Simplified Issue Term | No | THC disclosure still required; narrower carrier pool | Users who prefer no exam; rates slightly higher |

| Guaranteed Issue Whole Life | No | No health questions; no THC test | Daily users with other health conditions; coverage caps typically $25K–$50K |

| Group Life (Employer) | No | No individual underwriting; no cannabis questions | Any usage level; limited portability |

For most healthy marijuana users seeking meaningful death benefit coverage, such as $250,000 to $1M or more, a fully underwritten term life insurance policy with a marijuana-friendly carrier is commonly the most affordable option.

FAQs

Not automatically, but it often triggers deeper underwriting because the marijuana card signals an underlying health condition. In many cases, the diagnosis (pain disorder, seizures, cancer history, PTSD, anxiety) drives the life insurance rates more than cannabis itself. The best strategy is accurate disclosure and carrier selection that matches the medical narrative.

Typically, no. Most hemp-derived CBD products (under 0.3% THC) are not treated as tobacco use by life insurance companies and do not automatically trigger smoker rates.

However, full-spectrum CBD can contain trace amounts of THC. With frequent use, this may result in detectable THC on an insurance medical exam, depending on lab sensitivity and individual metabolism. A positive THC result does not automatically mean smoker rates, but disclosure must align with lab findings.

If you use marijuana recreationally or as a sleep aid and your frequency is low (1–4 times per month), carriers like Lincoln Financial and Prudential may still offer Preferred or Standard Non-Smoker classification. If your anxiety is severe, requires additional prescription medication, or has led to hospitalizations or time off work, the anxiety itself becomes the underwriting focus regardless of marijuana involvement.

Detection windows vary significantly by individual metabolism, body fat percentage, hydration, and frequency of use. In general, single or very occasional use may clear in 3–5 days; moderate use (several times per week) typically clears in 10–21 days; and daily or heavy use can be detectable for 30–60+ days. Hair follicle testing, used by some carriers, can detect THC for up to 90 days. The correct strategy is not to try to beat the test; it is to disclose accurately and let carrier selection do the work.

Yes. Simplified issue and accelerated underwriting term policies are available from several carriers and do not require a traditional insurance medical exam. However, these applications still ask about marijuana use on the health questionnaire, and some run a background check through the MIB and prescription databases.

If you’re aiming for the lowest possible life insurance premium, fully underwritten term life insurance often still wins, especially if your labs and vitals are strong.

Switching from smoking marijuana (inhalation) to edibles can improve how an underwriter views respiratory risk, especially if there’s any cough/bronchitis history. It does not erase frequency risk. Many carriers are more tolerant of ingestion than inhalation at the same usage level, but underwriting varies.

Switching from smoking marijuana (inhalation) to edibles can improve how an underwriter views respiratory risk, especially if there’s any cough/bronchitis history. It does not erase frequency risk. Many carriers are more tolerant of ingestion than inhalation at the same usage level, but underwriting varies.

This is an important and underappreciated question. Life insurance policies are contracts based on your health status at the time of application. If you are issued a Preferred Non-Smoker policy as a non-user and begin using marijuana afterward, you are not required to notify your carrier, and your existing coverage and life insurance premium are locked in. However, if you apply for additional coverage or a new policy, you will need to disclose current use at that time.

Underwriting guidelines are national. Carriers do not currently apply different standards based on whether cannabis is recreationally legal in your state. However, the legal environment does affect medical marijuana documentation.

The Bottom Line: Positioning Your Application for Success

Life insurance for marijuana users in 2026 is not the obstacle it once was, but it does require a strategy. The key principles:

- Disclose fully and accurately. The contestability risk of non-disclosure far outweighs any premium benefit.

- Frequency and method matter enormously. A twice-monthly edibles user and a daily cannabis smoker occupy very different underwriting universes.

- Carrier selection is the most powerful variable. The same applicant can receive Standard Non-Smoker at one carrier and Standard Smoker at another. This is why an independent broker who knows current marijuana underwriting guidelines across multiple carriers is essential.

- Your overall health profile is your strongest asset. Excellent blood pressure, healthy BMI, no tobacco, no DUI, and a clean medical history will all work in your favor regardless of cannabis use.

- Consider the consumption method. If you use it primarily for recreational or wellness purposes and are flexible on method, non-inhaled options generally produce the most favorable underwriting outcomes.

The goal is affordable life insurance that actually pays, and it starts with a well-positioned, fully honest application submitted to the right carrier.

For personalized guidance, consult a licensed independent life insurance broker with demonstrated experience in marijuana underwriting. Rates, carrier guidelines, and state regulations are subject to change.